As a CEO, if you were asked to show your company’s strategic plan, what would it look like? If like most, it’s around 20 pages, then it’s not a strategic plan – it’s an operations manual for your existing business.

Let’s start with a truism: innovation is important in every industry because every industry changes over time. To be successful in the future, companies need to adapt to that change or be that change.

If we assume that change is synonymous with innovation, then strategy is simply leadership in the future. If you’re not innovating, then it’s unlikely you’re being strategic.

Thomas Edison is attributed as having said, “Innovation is 1% inspiration and 99% perspiration.” By following the 2-Step Framework outlined below, business leaders can ensure their companies continue to be at the forefront of their industry. Businesses must innovate, either to defend against or be the industry disruption and execute those innovations by altering, where necessary, their firm’s business model.

First, separation

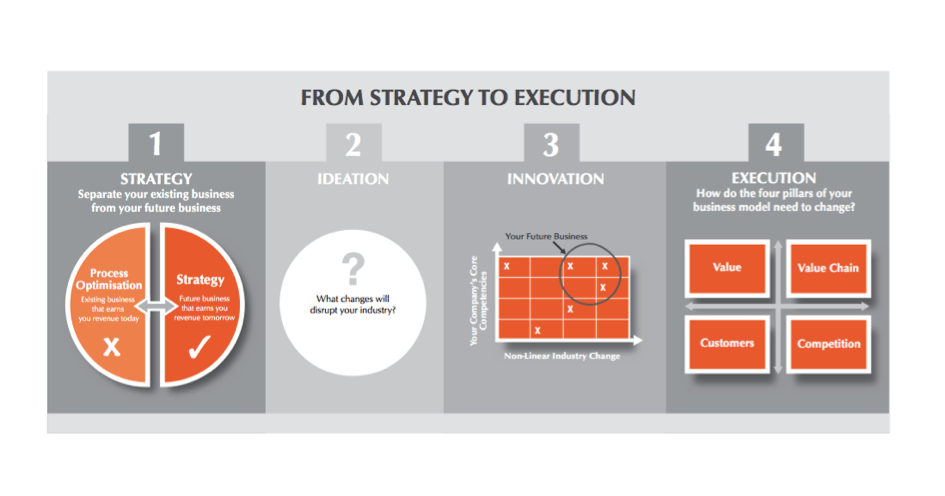

The first thing companies should do is to split their existing business from potential future businesses.

Existing businesses are what companies already do well: it’s what they earn revenues from today, and any improvements here can be called ‘process optimisation.’

What we’re interested in, however, is strategy: how will you generate revenue with your existing or new business tomorrow? How will you ensure your company’s future a decade from now?

To do this, leaders should consider building a separate team, adequately resourced and with an independent mindset – separate from the prevailing mindset within the company – to answer the following questions:

- What major disruption (non-linear change) will affect your industry?

- What will be the emergent changes in technology, customer preferences and competition trends in your industry?

After all, it’s not about what you do differently in the future, it’s about what you do differently today.

It’s imperative that this team is comprised of both your top-performers as well as an independent, objective third party. It’s highly unlikely they’ll be able to challenge the status quo if they created it. Kodak, Xerox and Blockbuster are all examples of companies that failed, not because they lacked the right strategic resources, but because they were too insular and as a result, did not adapt to non-linear industry disruptions until it was too late.

Think of Descartes’ rhetorical question, “How many kings started revolutions?” Independent objective 3rd parties are not ingrained with your firm’s dominant logic: they are not familiar with existing processes, have not developed an emotional attachment to the existing way of doing things and are therefore better suited to identifying new opportunities and finding new ways for your company to adapt to industry change.

After imagining the likeliest disruptive changes to your industry, managers should create a matrix and plot those changes against your company’s core competencies: your future business lies where industry change collides with your company’s key core competencies.

Second, execution (by focusing on business model adaptation)

The aforementioned processes of ideation and innovation shouldn’t be difficult. In fact, such exercises should be fun for those involved. Executing the identified and agreed upon changes is a different proposition entirely.

Execution is the single biggest reason innovation projects fail. Companies can overcome this by greatly simplifying the process and focusing on how existing key strategic resources will be utilised to execute changes and create a new business. This can be achieved through a process known as backcasting, or ‘folding-back’ the visualisation of the future to today and then focusing exclusively on the first 10% (and subsequently the next 10% and so on). Flexibility is key because the future is unknown and the pace of technological change is unprecedented.

To stay focused at every phase of execution, companies need to understand the key elements of their existing business model and understand how it needs to change. One way to do this is to list the four primary pillars that make up your firm’s business model, analyse which of them need to change, and then build a clear tactical roadmap around how those pillars will change. Such a roadmap can be built by answering the following questions, based around the standard pillars of a multi-industry business model:

- Value:

- What is the value of the new business?

- How will your new products and services increase the value being delivered?

- Value Chain & Distribution:

- How is the new value being delivered to the customer?

- Will the current value architecture have to change?

- Will there be significant changes in go-to-market approaches in the future?

- If the change is technology focused, will the new value be delivered through a product or a platform?

- Customers:

- Are today’s most profitable customers likely to be the same in the future?

- Who will your customers be in the future?

- Which non-consumers today could become consumers in the future?

- How will you find and convert them?

- Competition:

- How are your competitors reacting?

- Will they still be the same competitors in 10-15 years?

- Is a non-linear innovation coming from a new industry entrant?

- What are potential regulatory reforms?

A good example of a company that successfully executed industry innovation is Dell. The firm focused on key aspects of the standard industry business model in personal computers while serving the same customers and delivering the same value as its competitors (i.e. home computers). It fundamentally changed its value chain and distribution by focusing on design, manufacturing and the end-customer only, while removing the wholesale-retail component.

In summary, change is synonymous with strategy because strategy is leadership in the future and all industries are constantly in flux. To adapt to these changes, executives should split their existing business from a potential business that will generate revenue in the future. To imagine what this future business might be, it is important to create a new team partly staffed with an independent, objective third party that is not invested with your firm’s dominant logic or any existing processes. Your new business will exist where industry disruption meets your key competencies. To execute the required changes, leaders should simplify as much as possible by backcasting and focusing on the key pillars of their business model.