Photo by imagesthai.com from Pexels

Over the past decade, we’ve surveyed founders, next gens, and CEOs of family-owned firms. Their responses over time have underscored several evergreen qualities that we see in the family businesses we work with: an entrepreneurial spirit, a commitment to community, a focus on long-term strategic thinking and legacy. But conversely, an inattentiveness to succession planning was a common characteristic, which speaks to the overall theme of this year’s report: The missing middle: Bridging the strategy gap in US family firms.

By “missing middle,” we mean the gap between two visions – the entrepreneurial vision that sparks the formation of a business, and the long-term vision that allows family firms to pursue strategic goals far into the future. Companies that can bridge this gap are better positioned to secure their business and achieve bottom line growth. Our report highlights the following four areas to pay attention to for sustaining a profitable and purposeful family business operation.

Succession Planning

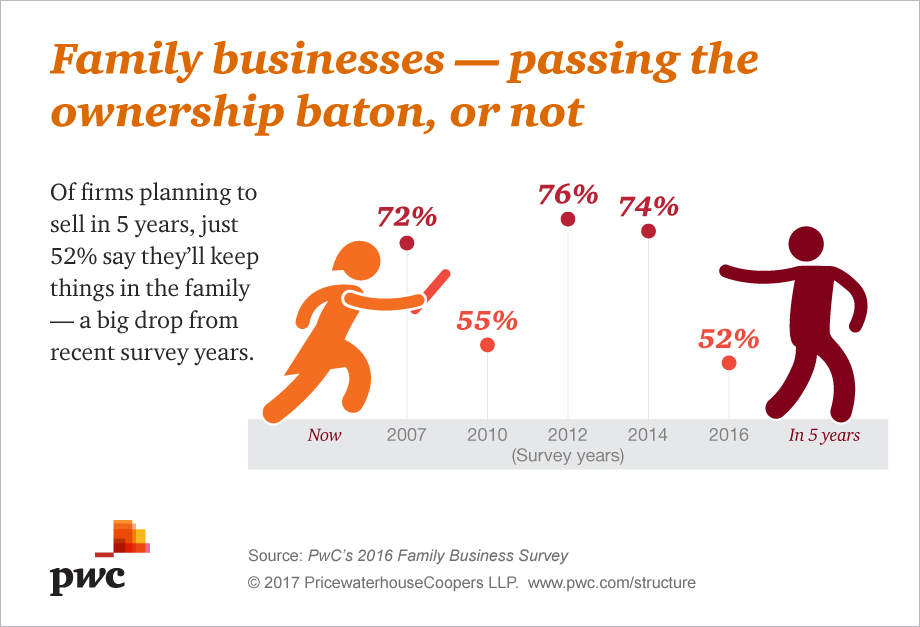

Just 23 percent of the family firms say they have a strong, documented succession plan in place, even fewer than two years ago. This is, in large part, because robust planning goes well beyond choosing a successor. It involves grooming that successor throughout the medium term — the gap between now and the eventual changing of the guard. This is especially important in the event that the current owner suddenly needs to transfer control of the business.

Take, for example, President-Elect Trump, who now has to pass control of his business to his children. We see other family businesses, particularly in their first generation of ownership, deal with similar issues when, like President-Elect Trump, much of their life has been spent building the business, with their personal identity is closely tied to it.

Take, for example, President-Elect Trump, who now has to pass control of his business to his children. We see other family businesses, particularly in their first generation of ownership, deal with similar issues when, like President-Elect Trump, much of their life has been spent building the business, with their personal identity is closely tied to it.

Within succession planning, there is another critical gap to bridge — the gender gap. A distressingly low 10 percent of our survey respondents were women, reflective of the overall number of women helming family firms. Currently, just 64 percent of family firms say that females and males in the next generation will be considered equally for leadership positions. Diversification of gender is key – especially on boards. Recent research shows that companies with more women in leadership roles generally have a greater focus on corporate governance.

Strategic Planning and Diversification

Greater emphasis on strategic and medium-term planning is another missing piece that would allow many family firms to achieve greater success and longevity. While an owner may often have a plan in his or her head, they don’t have a clearly written and communicated plan, which contains agreed upon vision and values, which can be a recipe for failure. For family businesses that do want continued success in this dynamic business environment, it’s important to focus on setting business goals over the medium term and deciding the direction of the firm.

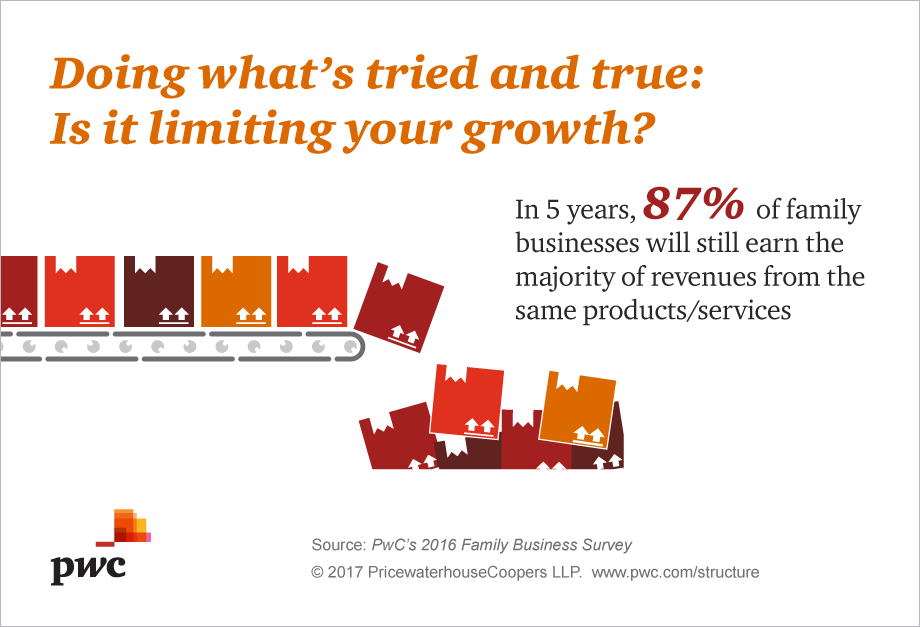

What we see in the survey data is that younger companies are being much less bullish than their mature counterparts when it comes to key medium-term strategies for sustaining strong growth in the long term. Chief among critical growth strategies missing from the middle here are diversification — a strategy for thriving well beyond a company’s next generation, in the face of industry disruption. Family businesses that expect double-digit growth in the next five years have a greater appetite for diversification, with 41% of them saying they’ll achieve that growth by expanding into new industry sectors.

Innovation

Just 21 percent of family firms we spoke with rank “being more innovative” as a very important business goal. Comparing this number with the 67 percent of firms that prioritize “ensuring the long-term future of the business” shows a disconnect between the current moment and the long-term future, and is a prime example of the missing middle. We heard more evidence of the missing middle when less than half of family firms told us they have a strategy fit for the digital age. Without such a plan, keeping pace with digital and emerging technology is likely to be difficult, and these firms could be blindsided by industry disruptors and more digitally savvy competitors.

The Talent Gap

The Talent Gap

The Talent Gap

The Talent GapFor family firms to innovate and achieve longevity, they need the right talent on board. Nearly half of family firms say they think they must work harder than other types of companies at acquiring talent equipped to help companies thrive in the changing economic landscape. This may be due to outside talent assuming there’s less opportunity at family businesses, since family members may appear more likely to take the choicest roles on the management team and be better poised for top leadership positions.

To combat this perception, family firms should diversify their talent base across multiple avenues. A critical best practice is maintaining a board with independent directors, family members and a strong chair. Diversification must also be prioritized when it comes to type of experience, expertise, technical knowledge, and professionalism.

The Bottom Line

Family firms remain a vital part of the US economy, but as they look to the future they must be agile in order to succeed. This means anticipating what’s far over the horizon while actively focusing on the middle-distance, reevaluating their succession plan and pipeline, prioritizing talent diversification, and taking innovation seriously.

To learn more about how to tackle the missing middle and obtain additional findings from our Family Business Survey, click here.

Written by Jonathan Flack, US Family Business Services Leader, Partner, Private Company Services at PwC.

Multigenerational History of The Scrooge Group")