Innovation is recommended by many but only truly executed by few. In order to understand how family businesses can become successful innovators, it is essential to understand the family business itself. By nature family businesses in the Middle East have many competitive advantages because of their unique combination of resources, their implied trust between stakeholders, and their long-term strategic vision. Undoubtedly, these families have shown that they know how to make money; the real question is whether they are also creating value. Mohamed Tahiri, Engineer & MBA from UCLA & IE Business School, entrepreneur and innovator with the Tahiri Family in Morocco (operating in import, manufacturing and distribution of plastic sandals, and real estate), explains why family businesses are uniquely placed to enable innovation, what they can change and how they can gain competitive advantages.

The word ‘innovation’ originally stems from the Latin word ‘innovare’, which stands for ‘to renew or to change’. In this article we explore how family businesses can understand and incorporate innovation and why it is important for value creation.

When family businesses orient themselves towards innovation, they may not be aware of the fact that they already hold a considerable competitive advantage over other companies. Large non-family companies encounter two obstacles when it comes to innovation: First, they are strongly influenced by their past in their present and future decision-making. What they experience is what is called in strategy “Path Dependency”, or being anchored by the decisions that made them successful in the past, even if the circumstances are not relevant anymore. Secondly, through that path-dependency large companies fail to undertake ‘disruptive innovation’. As opposed to ‘sustaining innovation’ which improves on existing products and services, disruptive innovation requires an entirely new value proposition (new product or service for a new customer segment) that might not always be aimed at the main existing customer segment of a company and therefore would be more difficult to implement, in an environment of short term vision, and constant pressure from the shareholders, and the financial market to manage these issues successful international companies look for innovation outside. For instance, Google is viewed as a highly innovative company, however, most of the ground-breaking innovation comes from outside; the company buys small start-ups that comprise innovative products and services.

It can be argued that both these obstacles present themselves to a lesser extent in family businesses. Often they do not have to answer to external shareholders and, therefore, can have a more long-term vision. Moreover, through the mix of generations that are managing the family business, path-dependency might be lessened, and therefore innovation might be easier to implement once the necessary mindset is acquired.

The drivers of innovation in family businesses

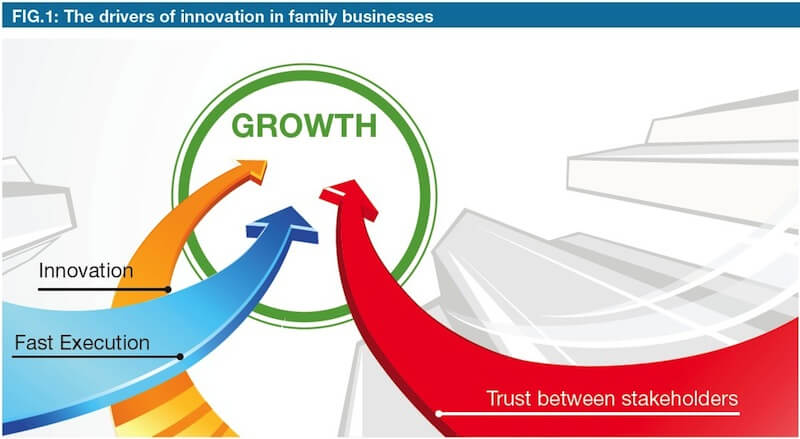

We can generally state that growth for any company depends on the combination of the following three factors (See Figure 1 below):

- Innovation

- Fast Execution

- Trust between stakeholders

Value is created only if these three factors are present. Family businesses generally do not have big issues with trust between stakeholders as they are known for their strong ties not only amongst family members but also with their suppliers and communities. However, families often find realising the other two factors somewhat more difficult. This brings us invariably back to the required mindset and culture of a company that will lead to innovation.

In order to assess the financial success of a family businesses we should not question whether the company is making money, but rather whether the company is making enough money compared to the risk that it is taking. The only way for a family business to make above average returns, and outperform the competition is by making sure that the three components of innovation, fast execution, and trust are combined. If the management is not able to produce above average returns, the shareholders are generally better off by investing in the stock market.

The change that is needed

Middle Eastern family businesses are said to be quite set in their ways and to adhere to traditions and customs. This has served most of them very well as through conservative approaches to risk and business the family legacies have been preserved over several generations. However, in order to take the business to the next level and to be able to credibly incorporate innovation as a strategy, family businesses have to change in the following respects:

A Culture of purpose: For years and years we have been taught that we should and can motivate employees. Yet, in real life, the truth is that we do not have the ability to motivate others; we can, however, inspire them. Inspiration can only come from sharing a sense of meaningful purpose throughout all the layers of an organisation. Having a vision is not enough to ensure that a family business can foster innovation; it needs a meaningful purpose and to lend a purpose credibility a company requires the right leadership. By meaningful purpose I mean any change that has a positive and great impact on our society, and that makes all stakeholders proud of their contribution.

The way we measure success: If the business measures success by how much money is made, it might quell the risk-taking that is sometimes necessary to evoke change and innovation cannot prosper. If success, however, is defined by the value, and the impact on the society that the company creates, then the whole mentality changes. According to Steve Jobs, Co-Founder and Chairman of Apple, one of the most important relationships in our lives is the one we have with money. As long as we keep money in its proper place and only see it as a tool or a commodity to achieve something that will have a positive impact on our society, we will be able to drive innovation and create value.

The relationship with risk and failure: Unfortunately, in oriental culture and family businesses especially, risk is never perceived as a learning opportunity. Of course, taking unnecessary risks is never encouraged, and we should always do our homework and due diligence. However, when we assess risks we tend to ask the question ‘What if I fail?’ while instead, a much more interesting question would be ‘What is the cost of failure?’. If the cost of failure is relatively low and the time it lasts is short, companies should proceed and take the risk. The most important thing is to assess that the recovery from failure is faster than that of other competitors. Family businesses should start thinking like venture capitalists: if two out of ten projects succeed and yield what they wished for in profit, then that is an excellent outcome. The failure of the other eight becomes relative.

Careful with social contracts: That there are certain social contracts is true for any society: Pressure from failure, and pressure to have the resources needed before seizing an opportunity. Maybe in oriental culture these contracts are still somewhat stricter than in Western culture. Many companies, for instance, stop short of innovation because they feel they do not have the resources and capabilities to start the processes needed. My professor George Geis at UCLA always said: ‘Entrepreneurship is the pursuit of opportunity beyond the resources you currently control.’George Bernard Shaw once said ‘The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man.’ Family businesses should try and move away from the mentality that all the resources need already be in place before they undertake a project.

Not about R&D: Many make the mistake of measuring innovation by how much a company invests in R&D. It is always about the people that work for the company and the way they are led. IBM used to spend much more on R&D than Apple and it still did not provide them with the competitive edge they needed to outdo their competitors. Innovation is not reserved to a new product development but can come from any function for instance, marketing, distribution, production, or finance.

The way we appraise performance: In family businesses in the Middle East, people only get fired because they fail to do their job. No one ever gets laid off because they missed an opportunity or failed to produce a new business idea. If innovative and forward thinking is not a part of an employee’s appraisal the danger of complacence and the suffocation of new ideas inevitably ensues. New performance appraisals should be installed in family businesses that value innovation.If family business can successfully implement these changes then the road towards sustainable innovation and the creation of value becomes clear. Businesses should understand that change is the only constant in today world from which they can gain.

How to stimulate innovation

Once a family business has acquired the mindset for change, there are a few things it can do to stimulate innovation and fast execution:

Diversity in people and industries: Hiring people from different industrial backgrounds can stimulate innovation enormously. Indeed, we often see that the biggest innovation in industry A can be provided by people that have a background in industry B. This leads us to realise that the future is already here, it is just not very evenly distributed, as William Gibson said. Sometimes this means that if we want to innovate in the automotive sector that we might want to look at the progress in the pharmaceutical industry for inspiration. Experience has shown that the results can be surprising.

Partner with international companies: Another way to stimulate innovation for Middle Eastern family businesses, is to partner with international companies. Here we need to make a distinction between the partnerships that are based on franchises and agency agreements and those that produce knowledge transfer. Innovation in partnerships will only be motivated if there is a shared purpose.

Investment in innovation: Family businesses, especially in the MENA should invest in start-ups and incubator processes. There are a lot of companies in Europe and the US, as well as the Middle East itself that are short of financing and would represent great investment opportunities.

Partner with connectors: In order to successfully make innovation known, a company needs people with relationships and communication skills that share the common purpose. This is very tricky because the communication that is needed is targeted at disseminating the innovation inside as well as outside the company. Thus, we need to find people that can connect internal as well as external stakeholders.

Allocate innovation-time: We have to create space and time for innovation to take place. Google employees, for example, have to allocate 20% of their time to innovation activities that have nothing to do with their day-to-day jobs. It is not optional; they have to allocate that time to new ideas. Engaging employees in this way increases the chances for sustainable innovation.

Review the processes: In order to enable innovation the family business has to make sure that its processes are optimised. They have to be efficient and up to date or else they can inhibit the realisation of new ideas and opportunities.

Question everything: There is no room for complacency in running a family business or any business for that matter. The family has to keep questioning what they do and what they believe in, even the very essentials of the businesses. There is a great lack of that questioning mentality in family businesses even though it is a great tool towards fostering innovation.

Bottom Line

When a company embraces an innovative mindset, it is still not guaranteed that innovation will ensue. Many innovative thinker never get anything done. Indeed, in order to succeed a company cannot stand still at an innovative attitude but has to become an innovative executer. In other words, it has to acquire the third factor towards value creation fast execution. In the end, innovation and value come from doing common things uncommonly well.

In family businesses the young generation can contribute much to bringing about innovation and fast execution. In fact, they are the key towards new ideas and approaches. Young family members are often not burdened with the path-dependency and have less difficulty in questioning existing paradigms. They are not scared of challenging core values, which to a certain measure can be beneficial. Of course, they must be well-educated, preferably abroad, and have external work experience. In order to be able to convince the older generation of their new ideas, young family members have to be able to demonstrate convincingly how value is added in the long run, and learn how to manage the resistance to change.

Tharawat Magazine, Issue 12, 2011